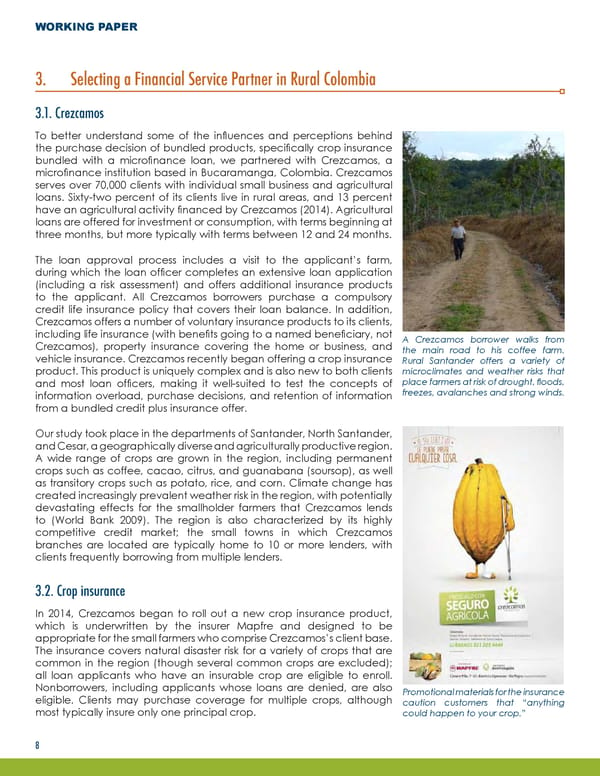

WORKING PAPER 3. Selecting a Financial Service Partner in Rural Colombia 3.1. Crezcamos To better understand some of the influences and perceptions behind the purchase decision of bundled products, specifically crop insurance bundled with a microfinance loan, we partnered with Crezcamos, a microfinance institution based in Bucaramanga, Colombia. Crezcamos serves over 70,000 clients with individual small business and agricultural loans. Sixty-two percent of its clients live in rural areas, and 13 percent have an agricultural activity financed by Crezcamos (2014). Agricultural loans are offered for investment or consumption, with terms beginning at three months, but more typically with terms between 12 and 24 months. The loan approval process includes a visit to the applicant’s farm, during which the loan officer completes an extensive loan application (including a risk assessment) and offers additional insurance products to the applicant. All Crezcamos borrowers purchase a compulsory credit life insurance policy that covers their loan balance. In addition, Crezcamos offers a number of voluntary insurance products to its clients, including life insurance (with benefits going to a named beneficiary, not A Crezcamos borrower walks from Crezcamos), property insurance covering the home or business, and the main road to his coffee farm. vehicle insurance. Crezcamos recently began offering a crop insurance Rural Santander offers a variety of product. This product is uniquely complex and is also new to both clients microclimates and weather risks that and most loan officers, making it well-suited to test the concepts of place farmers at risk of drought, floods, information overload, purchase decisions, and retention of information freezes, avalanches and strong winds. from a bundled credit plus insurance offer. Our study took place in the departments of Santander, North Santander, and Cesar, a geographically diverse and agriculturally productive region. A wide range of crops are grown in the region, including permanent crops such as coffee, cacao, citrus, and guanabana (soursop), as well as transitory crops such as potato, rice, and corn. Climate change has created increasingly prevalent weather risk in the region, with potentially devastating effects for the smallholder farmers that Crezcamos lends to (World Bank 2009). The region is also characterized by its highly competitive credit market; the small towns in which Crezcamos branches are located are typically home to 10 or more lenders, with clients frequently borrowing from multiple lenders. 3.2. Crop insurance In 2014, Crezcamos began to roll out a new crop insurance product, which is underwritten by the insurer Mapfre and designed to be appropriate for the small farmers who comprise Crezcamos’s client base. The insurance covers natural disaster risk for a variety of crops that are common in the region (though several common crops are excluded); all loan applicants who have an insurable crop are eligible to enroll. Nonborrowers, including applicants whose loans are denied, are also Promotional materials for the insurance eligible. Clients may purchase coverage for multiple crops, although caution customers that “anything most typically insure only one principal crop. could happen to your crop.” 8

Responsible Bundling of Microfinance Services Page 10 Page 12

Responsible Bundling of Microfinance Services Page 10 Page 12