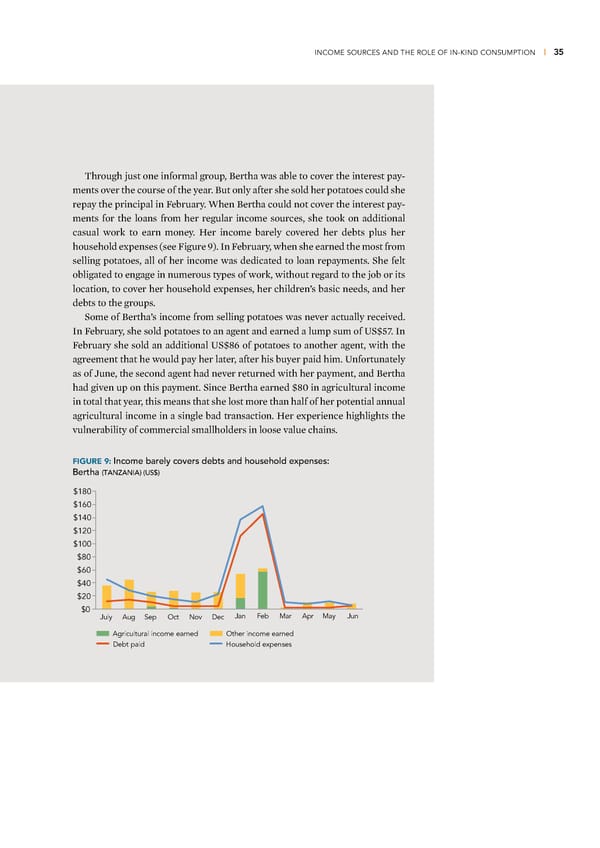

INCOME SOURCES AND THE ROLE OF IN-KIND CONSUMPTION | 35 Œhrough „ust one informal group, £ertha was able to cover the interest pay- ments over the course of the year £ut only after she sold her potatoes could she repay the principal in ebruary ™hen £ertha could not cover the interest pay- ments for the loans from her regular income sources, she too on additional casual wor to earn money Her income barely covered her debts plus her household expenses (see igure ž) €n ebruary, when she earned the most from selling potatoes, all of her income was dedicated to loan repayments She felt obligated to engage in numerous types of wor, without regard to the „ob or its location, to cover her household expenses, her children’s basic needs, and her debts to the groups Some of £ertha’s income from selling potatoes was never actually received €n ebruary, she sold potatoes to an agent and earned a lump sum of ©S±”• €n ebruary she sold an additional ©S±¡¢ of potatoes to another agent, with the agreement that he would pay her later, after his buyer paid him ©nfortunately as of Žune, the second agent had never returned with her payment, and £ertha had given up on this payment Since £ertha earned ±¡’ in agricultural income in total that year, this means that she lost more than half of her potential annual agricultural income in a single bad transaction Her experience highlights the vulnerability of commercial smallholders in loose value chains FIGURE 9: Income barely covers debts and household expenses: Bertha (TANZANIA) (US$) $180 $160 $140 $120 $100 $80 $60 $40 $20 $0 Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec Agricultural income earned Other income earned Debt paid Household expenses

Financial Diaries with Smallholder Families Page 47 Page 49

Financial Diaries with Smallholder Families Page 47 Page 49